How to value R&D spending in a company: The invisible value

This post presents how to consider R&D spending in a company as an investment instead of spending.

This post presents how to consider R&D spending in a company as an investment instead of spending.

The material is derived from [1]. We highly recommend this reference book for reader to read. Note that this material is only available in the book published in 2011 instead of the latest print edition.

R&D spending is an invisible investment which often being overlooked by a company as a normal spending as others.

However, we should consider R&D as intangible asset as well as capital expenditure covering multiple years (typically 10 years as when we use to value a company in the period of 10 years) instead of operating expenditure within a single year.

Let’s have a brief discussion about the value of R&D in a company.

READ MORE: Research how to: A practical guide

R&D is an intangible asset

Unlike in the past where manufacturing and railways companies usually were the biggest profitable business, in current day and age, the largest profitable companies are typically technology companies which offer software and service systems.

These large technological companies, most of the assets are not in the form of building, machinery and material. Instead, those large technological companies have intangible assets including human capital (skills and knowledge), technology or system, cloud infrastructure as well as brand as their main assets.

That is, most of the value of those technological companies comes from intangible assets.

These intangible assets (R&D resources and activities covering human capital, technology, brand and others) have important contributions for the value of a company.

To value R&D activities we should appropriately place R&D expense following the first principle in accounting.

In accounting, there are two main types of expenditures as follows:

- Operating expenditure is an expense which generate benefits for the current year (within 1 year).

- Capital expenditure is an expense which create multiple year benefits.

R&D activities are capital expenditure instead of operating expenditure!

By considering R&D as capital expenditure, we can adjust the calculation of the operating income, net income and equity of a company.

R&D expenses include development expenses (such as materials, equipment and facilities), recruiting talent, training people and other activities contribute to R&D related activities.

The first step to value R&D activities is by checking the income and balance sheet statements of a company and find the total capital expenses related to R&D activities.

R&D expense is a capital investment!

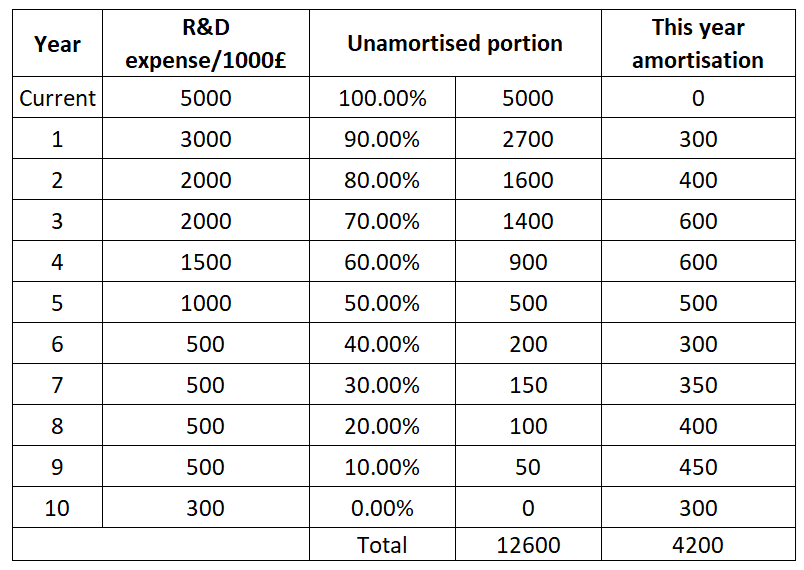

We can illustrate this by considering a company A which has R&D expenditure for 10-year cycle as shown in Table 1 below.

In this R&D expenditure example, we assume 10% of the expense is amortised (similar to depreciation on physical assets such as building and factory) each year.

From Table 1, during the period of 10-year, the total unamortised R&D expenses (the expense that give benefits to the company in the form of product or service improvements) is £12600 thousand. The current year R&D expense is £5000 thousand.

Meanwhile, the total amortised R&D expense during the period is £4200 thousand.

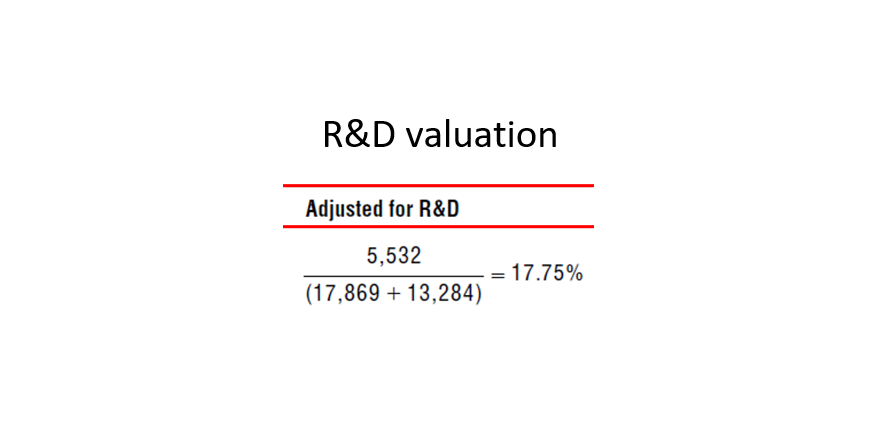

Hence, we should consider these total unamortised and amortised R&D expenses and current year R&D expense in the total equity, operating income and net income as follows [1]:

- Adjusted book value of equity: Stated book value of equity + total R&D capital expenditure.

- Adjusted operating income: Stated operating income + R&D capital expenditure in the current year– total amortised R&D.

- Adjusted net income: Stated net income + R&D capital expenditure in the current year – total amortised R&D.

Suppose the company A has stated book value of equity = £20000 thousand, operating income = £5000 thousand and net income =£3000 thousand.

Hence, by considering R&D as capital expenditure (and investment), the adjusted values of them become:

- Adjusted book value of equity: (£20000+£12600) thousand = £32600 thousand.

- Adjusted operating income: (£5000 +£5000-£4200) thousand = £5800 thousand.

- Adjusted net income: (£3000 +£5000-£4200) thousand = £3800 thousand.

From this example, we can observe by valuing R&D as capital expenditure and hence as investment, we can have higher actual equity, operating income and net income values compared when we consider R&D only as typical operating expense.

In addition, capital expenditures from R&D as investment also lower the P/E ratio of a company making the share of the company to have lower price (increasing the probability that the company is undervalued) compared when R&D is not considered [1]!

For example, if a public company has a P/E ratio of 14.62. When R&D is valued, the adjusted P/E ratio = P/(E+R&D) may become, for example, 9.43.

With this lower adjusted P/E value, there is a possibility that the company is actually under-valued instead of over-valued!

In summary, R&D activities provide invisible values to a company.

READ MORE: Learning resiliency and modern invention from James Dyson

Conclusion

In this post, we briefly discussed how R&D spending contributes an important role in the value of a company.

This is very relevant especially currently large companies are companies based on technology which do not have large physical assets like factories or materials.

The fundamental step is by considering R&D related spending as capital expenditure instead of operating expense.

By considering R&D activities as capital expenditure, then we can adjust the real equity, operating income and net income of a company and properly value the company.

In summary, R&D increases the value of a company!

Reference

[1] Aswath, D., 2011. The little book of valuation.

You may find some interesting items by shopping here.